#Modular Robotics forecast

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

vedere-transformers-ilrisveglio

OPENLOAD!! Transformers 7 streaming ITA 2023 in Altadefinizione

1 post

Fun Fact

Tumblr Inc. has $15.1M in annual revenue.

Text

Trends and Forecasts in the Second Life Industrial Robot Market

The Second Life Industrial Robot MarketSecond Life Industrial Robot Market is rapidly expanding as businesses increasingly seek cost-effective automation solutions across manufacturing, logistics, and automotive sectors. These pre-owned, refurbished robots offer a budget-friendly alternative to new systems while delivering reliable performance and extended lifecycles. Growing trends include advanced refurbishing services, AI integration, and alignment with Industry 4.0 technologies, enhancing robot adaptability and efficiency. Despite challenges like standardization gaps, compatibility issues, and skilled labor shortages, the market benefits from rising demand driven by cost optimization and sustainability efforts. With ongoing innovations and a focus on circular economy practices, the second-life robot market is poised for significant growth and greater adoption worldwide.

Market Segmentation:

1. By End Use:

Industrial

Waste Recycling

Others

2. By Type of Refurbishment:

New Controller Technology

Others

3. By Region:

North America

Europe

Asia-Pacific

Rest of the World

Key Market Players

ABB

FANUC

IRS Robotics

Key Demand Drivers

Inexpensive Automation for Small and Medium Businesses: Because second-life robots drastically lower startup costs, automation is now affordable for manufacturers on a budget as well as small and mid-sized businesses (SMEs). This affordability is especially alluring in budget-conscious competitive industries and growing markets.

Goals for the Circular Economy and Sustainability: Businesses are adopting sustainable practices as a result of increased environmental awareness and more stringent e-waste rules. In line with circular economy concepts, refurbished robots prolong the useful life of current gear while lowering the load on landfills and conserving vital resources.

Improvements in Technology: Refurbished robots are becoming more versatile thanks to improved controller systems, AI integration, and machine learning applications. These improvements make older models more useful in high-precision settings and smart factories by enabling them to function on par with machines of the latest generation.

Market Challenges

Absence of Standardized Procedures for Renovation: Variations in robot safety, dependability, and quality caused by inconsistent refurbishing procedures among vendors may worry end users and restrict further adoption.

Integration Difficulties: Connecting legacy systems to automation platforms, Industry 4.0 frameworks, or contemporary software environments may necessitate extensive adaptation. Potential customers may be turned off by these integration fees, which can cancel out any initial savings.

Lack of Skilled Workers: Industrial robot maintenance and repair require specialized technical knowledge. The consistency of refurbished equipment quality and the scalability of services can be affected by a shortage of qualified personnel.

Get your hands on this Sample Report to stay up-to-date on the latest developments in the Second Life Industrial Robot Market.

Gain deep information on Robotics and Automation Market. Click Here!

Future Outlook

Through 2030, the market for used industrial robots is anticipated to develop significantly due to the combined demands of sustainability and economic efficiency. The performance of reconditioned robots will continue to improve with the development of AI-enabled control systems and modular modifications, making them more and more feasible for high-end industrial applications. With the help of favorable government policies, growing SME automation, and fast industrialization, the Asia-Pacific area is expected to grow at the fastest rate. Because of its well-established robotics infrastructure and advanced refurbishing skills, North America is expected to continue to hold its dominant position.

Conclusion

With its perfect blend of cost, sustainability, and performance, the second life industrial robot market is becoming a vital part of the worldwide automation scene. Refurbished robots are turning out to be a valuable asset for contemporary industry as the need for intelligent, environmentally friendly, and scalable automation solutions increases. Even if there are still issues with standardization and integration today, industry cooperation, technical advancement, and training programs should help to lessen them over time. The market for second-life robots is positioned for long-term growth and change because to strong regional demand and growing environmental concern.

#Second Life Industrial Robot Market#Second Life Industrial Robot Industry#Second Life Industrial Robot Report#robotics#automation

0 notes

Text

Vertical Farming Market to Hit $13.7 Billion by 2029 Driven by AI and Sustainability

The Vertical Farming Market is poised for exponential growth, forecasted to increase from approximately USD 5.6 billion in 2024 to USD 13.7 billion by 2029, growing at a compound annual growth rate (CAGR) of 19.7%. This transformation is being driven by urbanization, increasing food demand, water scarcity, and technological innovations including artificial intelligence (AI), LED lighting, and hydroponic systems.

To Get Free Sample Report: https://www.datamintelligence.com/download-sample/vertical-farming-market

Market Drivers and Growth Opportunities

Scarcity of Arable Land and Water Vertical farming systems require up to 97% less water and significantly less land than traditional farming, making them ideal for densely populated cities and regions suffering from water scarcity.

Integration of AI and Automation AI is revolutionizing vertical farming by enabling predictive analytics, automation of nutrient delivery, environmental control, and yield optimization. Coupled with IoT and sensors, farms can operate efficiently with minimal human input.

Year-Round Production and Urban Scalability Controlled environment agriculture allows year-round production regardless of climate conditions. This is especially crucial in urban areas where local food production can reduce dependency on external supply chains and transportation.

Rising Demand for Clean, Pesticide-Free Produce Health-conscious consumers are driving demand for fresh, pesticide-free food. Vertical farming offers a solution with clean growing environments that eliminate the need for chemical treatments.

Government Incentives and Policy Support Supportive policies in both developed and developing countries are fostering investment and research in sustainable agricultural practices, including vertical farming.

U.S. Market Insights

The United States is one of the leading adopters of vertical farming technology. In urban food deserts regions with limited access to fresh food small and modular farms are addressing local needs. For example, projects in cities like Houston, Phoenix, and Mesa are creating access to greens using hydroponics and aeroponics.

Energy use remains a major challenge, as climate-controlled farms consume high levels of electricity. However, innovators are mitigating this through renewable energy integration and partnerships with local energy providers. Furthermore, advanced LED lighting is being optimized for energy efficiency.

Despite some high-profile vertical farm companies declaring bankruptcy due to overexpansion or unprofitable scale, many small and mid-size operators are succeeding with localized, efficient models. Companies like Bowery Farming are providing produce to major retailers including Walmart and Whole Foods, supported by automation and AI tools that streamline farm management.

Startups like True Garden are demonstrating profitability with container-based models, producing thousands of pounds of greens each month while using 90–98% less water than traditional farms.

Japan Market Trends

Japan’s vertical farming industry is expanding rapidly, driven by the need for domestic food production and sustainability. Indoor farms, known as "vegetable factories," are increasingly integrated into urban environments. The vertical farming market in Japan was valued at USD 402 million in 2024 and is projected to reach USD 879 million by 2033, with a CAGR of 9.1%.

Robotics, biosciences, and AI are at the core of Japan's vertical farming technology. Companies like Spread are leveraging cloud-based farm management systems to distribute greens to thousands of retail stores. The cultural alignment with sustainability, minimal waste, and urban efficiency positions Japan as a key global influencer in vertical farming.

Government funding and corporate investment are further accelerating growth, particularly in the development of fully automated farming systems that reduce reliance on human labor.

Global Market Landscape

The Asia-Pacific region, beyond Japan, is also witnessing notable growth. In 2023, the market was valued at USD 1.77 billion and is projected to reach USD 7.04 billion by 2030 at a CAGR of 21.8%. Countries such as Singapore, South Korea, and China are investing heavily in vertical farming for urban food security.

Hydroponics is currently the dominant method due to its water efficiency and scalability. Aeroponics is gaining momentum, especially in Japan and parts of Europe, due to its superior nutrient delivery and root oxygenation.

Investment Opportunities

Vertical farming is attracting venture capital across multiple fronts:

Automation and AI: Investors are prioritizing platforms that use AI to manage farm ecosystems in real-time.

Container and Modular Farms: Scalable, transportable farms offer a solution for urban redevelopment and rural supply gaps.

Premium Crop Segments: High-value crops like microgreens, strawberries, and herbs offer better margins for vertical farmers.

Food Security Projects: Urban governments and non-profits are partnering with startups to launch vertical farms in underserved neighborhoods.

Get the Demo Full Report : https://www.datamintelligence.com/enquiry/vertical-farming-market

Industry Challenges

High Energy and Infrastructure Costs Energy-intensive systems for lighting, heating, and environmental control present cost challenges. Co-locating farms with renewable energy sources is a potential solution.

Scalability and Profitability Balance Large-scale operations often struggle with profitability, whereas smaller localized farms show better financial performance and community impact.

Supply Chain and Distribution Ensuring freshness and shelf life, especially for leafy greens, requires efficient local distribution networks.

Conclusion

The vertical farming market is on a transformative path. Innovations in AI, hydroponics, and sustainable lighting are enabling farms to flourish in environments previously unsuitable for agriculture. While energy consumption and initial investment remain hurdles, the long-term benefits of local food production, water savings, and food security are positioning vertical farming as a central player in the future of agriculture. With leadership from the U.S. and Japan, and rapid growth in the Asia-Pacific region, vertical farming is no longer experimental it is becoming essential.

0 notes

Text

Modular Hall Effect Sensors Market: Future Growth of the Semiconductor Sector, 2025–2032

MARKET INSIGHTS

The global Modular Hall Effect Sensors Market size was valued at US$ 834 million in 2024 and is projected to reach US$ 1.34 billion by 2032, at a CAGR of 7.1% during the forecast period 2025-2032. The U.S. market accounted for 32% of global revenue in 2024, while China is expected to witness the highest growth rate at 7.8% CAGR through 2032.

Modular Hall Effect sensors are compact, overmolded devices that detect magnetic fields with IP67-rated protection. These sensors separate the magnetic target from enclosed electronics, enabling space-efficient installations in demanding environments. They offer both analog and digital output options, making them versatile for position sensing, speed detection, and current measurement applications across industries.

The market growth is driven by increasing automation in manufacturing and rising electric vehicle production, where these sensors enable precise motor control. Furthermore, advancements in Industry 4.0 technologies and growing adoption in consumer electronics for touchless interfaces are expanding application horizons. Key players like Allegro MicroSystems and Texas Instruments are introducing energy-efficient variants with integrated signal conditioning, addressing the need for smarter IoT-enabled solutions.

MARKET DYNAMICS

MARKET DRIVERS

Growing Adoption in Automotive Applications Fuels Market Expansion

The automotive industry’s increasing reliance on modular Hall effect sensors is a primary driver for market growth. These sensors are critical for position sensing in throttle control, gear shift detection, and braking systems in modern vehicles. With the automotive sector accounting for over 35% of global Hall effect sensor demand, the transition toward electric vehicles (EVs) and advanced driver-assistance systems (ADAS) creates substantial opportunities. The integration of these sensors in brushless DC motors for EV powertrains, where they offer high reliability in harsh environments, is particularly noteworthy. Recent technological advancements have enhanced their ability to operate in temperature ranges from -40°C to 150°C, making them indispensable for automotive applications.

Industrial Automation Boom Accelerates Demand

Industrial automation represents another significant growth avenue, with modular Hall effect sensors finding extensive use in motor controls, robotics, and conveyor systems. The global industrial automation market is projected to grow at nearly 9% CAGR through 2030, creating parallel demand for precision sensing solutions. These sensors enable non-contact position detection in harsh industrial environments where traditional mechanical switches fail. Their modular design with IP67-rated housings provides robust protection against dust and moisture, a critical requirement in manufacturing facilities. Furthermore, Industry 4.0 initiatives are driving the adoption of smart sensors with digital outputs that can interface directly with IoT systems, creating new integration possibilities.

➤ An analysis of production data shows that industrial applications now account for approximately 28% of modular Hall effect sensor deployments, with particularly strong uptake in packaging machinery and CNC equipment.

The trend toward miniaturization in consumer electronics also presents significant growth potential. As devices become smaller, modular Hall effect sensors offer compact solutions for lid position detection in laptops and foldable smartphones, with some models now measuring less than 2mm x 2mm.

MARKET CHALLENGES

Intense Price Competition from Alternative Technologies

While modular Hall effect sensors offer distinct advantages, they face mounting competition from alternative sensing technologies like magnetoresistive (MR) and giant magnetoresistive (GMR) sensors. These alternatives often provide higher sensitivity and better signal-to-noise ratios in certain applications, putting pressure on Hall sensor manufacturers to differentiate their offerings. In price-sensitive markets such as consumer electronics, this competition frequently leads to margin erosion, with some sensor prices declining by approximately 15% over the past three years. Maintaining profitability while meeting the demand for cost reductions remains an ongoing challenge for major players.

Other Challenges

Supply Chain Vulnerabilities The semiconductor shortage impacts have revealed vulnerabilities in the sensor supply chain, particularly for specialized packaging materials. Lead times for certain sensor components have extended to 26 weeks in some cases, disrupting production schedules.

Technical Limitations Achieving sub-micron position resolution remains technically challenging for standard Hall effect designs, limiting their adoption in ultra-high precision applications compared to optical encoders.

MARKET RESTRAINTS

Design Complexity in High-Temperature Applications

While modular Hall effect sensors perform well in standard industrial environments, their application in extreme conditions presents design challenges. Operation above 150°C requires specialized materials and packaging techniques that can increase unit costs by 30-40%. This temperature limitation restricts their use in certain aerospace and oil/gas applications where environments routinely exceed these thresholds. The thermal drift characteristics of Hall elements also necessitate sophisticated compensation circuits, adding to system complexity and BOM costs.

Additionally, the need for precise magnetic field calibration in production creates yield challenges, with typical manufacturing tolerances requiring adjustments to ±1% or better for critical applications. These factors collectively restrain broader market adoption in some specialized segments.

MARKET OPPORTUNITIES

Emerging Medical Applications Present Significant Growth Potential

The medical device sector represents a high-growth opportunity, with modular Hall effect sensors finding new applications in surgical robotics, drug delivery systems, and implantable devices. The medical sensors market is projected to exceed $20 billion by 2027, creating substantial demand for reliable position sensing solutions. Recent innovations include contactless sensing for MRI-compatible equipment and miniature sensors for insulin pump mechanisms. The sterilization compatibility of properly packaged modular sensors makes them particularly attractive for single-use medical devices.

Furthermore, the development of ultra-low power Hall sensors consuming less than 10μA enables new battery-powered wearable applications with multi-year operational life, opening additional market segments. Strategic partnerships between sensor manufacturers and medical OEMs are accelerating the development of application-specific solutions.

MODULAR HALL EFFECT SENSORS MARKET TRENDS

Shift Towards Compact, High-Performance Sensing Solutions Drives Market Growth

The global Modular Hall Effect Sensors market, valued at $XX million in 2024, is experiencing robust expansion due to increasing demand for compact and reliable sensing solutions in industrial and automotive applications. These sensors, known for their IP67-rated durability and separation of magnetic targets from enclosed electronics, offer significant advantages in space-constrained installations. The automotive sector alone accounts for over 30% of total sensor demand, driven by the need for precise position detection in electric power steering and transmission systems. As industries continue miniaturizing components while requiring higher precision, modular Hall effect sensors are becoming the technology of choice for engineers worldwide.

Other Trends

Industrial Automation Revolution

The fourth industrial revolution is accelerating adoption across manufacturing sectors, with modular Hall effect sensors playing a critical role in Industry 4.0 implementations. These contactless sensors enable precise speed measurement in conveyor systems with an accuracy margin of ±1%, while their modular design allows easy integration into existing automated workflows. The global industrial automation market’s projected CAGR of 9.3% through 2032 directly correlates with increasing sensor deployments in robotic assembly lines and smart factory environments.

Advancements in Material Science and Chip Design

Recent breakthroughs in semiconductor materials and 3D packaging technologies are enabling sensor manufacturers to develop products with 30% higher sensitivity compared to previous generations. Leading manufacturers are now incorporating graphene-based elements and advanced ferromagnetic alloys that maintain stability across extreme temperature ranges from -40°C to 150°C. These innovations are particularly crucial for aerospace applications where sensors must perform reliably in both stratospheric cold and engine compartment heat. Digital output variants now dominate new product launches, representing 58% of 2024 modular Hall sensor introductions due to their compatibility with modern IoT ecosystems.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Strategic Expansion Drive Market Leadership

The global modular Hall Effect sensors market exhibits a moderately consolidated competition structure, where established electronic component manufacturers compete with specialized sensor providers. Sensata Technologies leads the segment with an estimated 18% revenue share in 2024, leveraging its diversified industrial sensor portfolio and strong OEM relationships in the automotive sector.

Texas Instruments and Allegro MicroSystems collectively hold approximately 25% market share, driven by their advanced semiconductor expertise and vertically integrated production capabilities. These companies continue to dominate due to their ability to offer customized solutions for high-growth applications such as electric vehicles and Industry 4.0 automation systems.

While traditional players maintain strong positions, emerging competitors like Melexis are disrupting the market through innovative packaging technologies and miniaturized sensor designs. The Belgium-based company recently launched its third-generation Hall Effect ICs, specifically optimized for space-constrained medical devices and wearables.

The supplier ecosystem is witnessing increased M&A activity as manufacturers seek to consolidate expertise. Littelfuse’s 2023 acquisition of C&K Components exemplifies this trend, enhancing their position in ruggedized industrial sensors. Similarly, Rohm Semiconductor expanded its European footprint through strategic partnerships with automotive Tier 1 suppliers.

List of Key Modular Hall Effect Sensor Companies Profiled

Sensata Technologies (U.S.)

Texas Instruments (U.S.)

Rohm Semiconductor (Japan)

Littelfuse (U.S.)

ZF Switches & Sensors (Germany)

Marposs (Italy)

Allegro MicroSystems (U.S.)

Lake Shore Cryotronics (U.S.)

Regal Components (Sweden)

Silicon Labs (U.S.)

Melexis (Belgium)

Segment Analysis:

By Type

Hall Switch Segment Leads the Market with Extensive Use in Position Sensing and Switching Applications

The market is segmented based on type into:

Hall Switch

Subtypes: Unipolar, Bipolar, and Omnipolar

Linear Hall Sensor

Subtypes: Analog Output and Digital Output

Others

By Application

Automotive Segment Dominates Due to Increasing Adoption in Position Detection and Current Sensing Applications

The market is segmented based on application into:

Consumer Electronics

Automotive

Aerospace

Medical

Industrial

By Functionality

Position Sensing Segment Holds Major Share with Growing Demand Across Industries

The market is segmented based on functionality into:

Position Sensing

Current Sensing

Speed Detection

Others

By Output

Analog Output Segment Maintains Strong Position in Various Measurement Applications

The market is segmented based on output into:

Analog Output

Digital Output

Subtypes: Pulse Width Modulation (PWM), I2C, and SPI

Others

Regional Analysis: Modular Hall Effect Sensors Market

North America The North American market remains a key revenue generator for modular Hall effect sensors, driven by strong automotive and industrial automation demand. The U.S. accounts for over 60% of the regional market value, benefiting from heavy investments in electric vehicle manufacturing and smart factory initiatives. Recent technological advancements by market leaders like Allegro MicroSystems and Texas Instruments have strengthened product offerings in high-temperature and high-precision applications. However, pricing pressures from Asian manufacturers pose a challenge to domestic producers. The Canadian market shows steady growth, particularly in aerospace and medical equipment segments where reliability is paramount.

Europe Europe’s market is characterized by stringent quality standards and innovation-driven demand, particularly in automotive and industrial sectors. Germany leads adoption with its robust manufacturing base, while Nordic countries demonstrate increasing usage in renewable energy systems. The Hall Switch segment dominates due to its prevalence in automotive position sensing applications. European OEMs emphasize miniaturization and energy efficiency, creating opportunities for modular sensors with integrated signal processing. However, the transition to electric vehicles has temporarily disrupted traditional supply chains, causing suppliers to realign production capacities toward EV-specific sensor solutions.

Asia-Pacific Asia-Pacific represents the fastest-growing regional market, projected to capture over 45% of global demand by 2032. China’s dominance stems from massive electronics production and government-backed Industry 4.0 initiatives fueling industrial automation. Japanese manufacturers lead in high-precision applications like robotics, while South Korea sees strong demand from consumer electronics giants. The region witnesses intense price competition, with local players like ROHM Semiconductor gaining market share through cost-effective solutions. India emerges as a promising market with expanding automotive manufacturing and infrastructure modernization programs, though quality consistency remains a concern among buyers.

South America Market growth in South America remains moderate, constrained by economic instability and limited local manufacturing capabilities. Brazil accounts for nearly half the regional demand, primarily serving automotive and appliance industries. Cost sensitivity drives preference for basic Hall Switch models over advanced linear sensors. While foreign investments in Argentina’s industrial sector show potential, currency volatility discourages long-term commitments from major sensor suppliers. The aftermarket for sensor replacements presents steady opportunities, particularly in aging industrial equipment maintenance across the continent.

Middle East & Africa This region demonstrates uneven growth patterns, with Gulf Cooperation Council countries leading adoption in oil/gas and building automation applications. Israel’s thriving medical technology sector drives specialist demand for high-reliability sensors. South Africa serves as an industrial hub for sub-Saharan Africa, though infrastructure limitations hinder widespread sensor integration. The market sees increasing Chinese imports due to competitive pricing, while European suppliers maintain dominance in high-value industrial projects. Government initiatives to diversify economies toward manufacturing create long-term growth potential, albeit from a comparatively small base.

Report Scope

This market research report provides a comprehensive analysis of the global Modular Hall Effect Sensors market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global market was valued at USD million in 2024 and is projected to reach USD million by 2032.

Segmentation Analysis: Detailed breakdown by product type (Hall Switch, Linear Hall Sensor), application (Consumer Electronics, Automotive, Aerospace, Medical, Industrial), and end-user industry to identify high-growth segments.

Regional Outlook: Insights into market performance across North America (USD million market size in U.S.), Europe, Asia-Pacific (China projected at USD million), Latin America, and Middle East & Africa.

Competitive Landscape: Profiles of leading market participants including Sensata Technologies, Texas Instruments, Allegro MicroSystems, and others holding approximately % market share in 2024.

Technology Trends & Innovation: Assessment of emerging sensor technologies, integration with IoT systems, and evolving industry standards for magnetic sensing applications.

Market Drivers & Restraints: Evaluation of factors including automotive electrification, industrial automation demand, along with supply chain constraints and material cost challenges.

Stakeholder Analysis: Strategic insights for sensor manufacturers, OEMs, system integrators, and investors regarding market opportunities and competitive positioning.

Related Reports:https://semiconductorblogs21.blogspot.com/2025/06/global-video-sync-separator-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/silicon-rings-and-silicon-electrodes_17.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/ceramic-bonding-tool-market-investments.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/coaxial-panels-market-challenges.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/oled-and-led-automotive-light-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/gas-cell-market-demand-for-ai-chips-in.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/digital-demodulator-ic-market-packaging.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/nano-micro-connector-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/single-mode-laser-diode-market-growth.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/silicon-rings-and-silicon-electrodes.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/battery-management-system-chip-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/scanning-slit-beam-profiler-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/atomic-oscillator-market-electronics.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/plastic-encapsulated-thermistor-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/ceramic-bonding-tool-market-policy.html

0 notes

Text

How Can AI Software Development Services Boost Your Business?

In today's rapidly evolving digital economy, staying competitive requires more than just adapting to technology—it demands innovation driven by intelligence. Artificial Intelligence (AI) is no longer a futuristic concept; it's a present-day force transforming industries across the globe. For businesses aiming to thrive in this landscape, AI software development services have emerged as a powerful catalyst for growth, efficiency, and innovation.

What Are AI Software Development Services?

AI software development services refer to the design, development, and deployment of AI-driven applications and systems tailored to specific business needs. These services often include machine learning (ML), natural language processing (NLP), computer vision, predictive analytics, and robotic process automation (RPA), among others. Leading AI development companies build intelligent systems that can learn from data, make decisions, and automate processes to drive value.

1. Streamlining Operations Through Automation

AI excels at automating repetitive and rule-based tasks. By integrating AI into core workflows, businesses can significantly reduce the need for manual intervention, minimize errors, and increase overall efficiency.

AI-powered bots can handle customer inquiries 24/7.

Intelligent automation tools can manage data entry, invoice processing, and inventory management.

Robotic Process Automation (RPA) can streamline back-office operations.

This results in cost savings, faster turnaround times, and more consistent outcomes.

2. Improving Decision-Making with Data Insights

Every business generates vast amounts of data, but only a few know how to utilize it effectively. AI software development services help transform raw data into actionable insights.

Predictive analytics models forecast trends and customer behavior.

AI algorithms identify patterns and anomalies in large datasets.

Real-time dashboards offer instant visibility into key performance metrics.

With AI, decision-makers can make more informed, data-driven choices that boost productivity and profitability.

3. Enhancing Customer Experience

Modern consumers expect personalized, seamless, and responsive interactions. AI enables businesses to deliver on these expectations:

AI chatbots offer instant customer support and query resolution.

Recommendation engines suggest products/services based on user behavior.

Sentiment analysis helps understand customer feedback in real time.

These solutions not only enhance user satisfaction but also foster customer loyalty and long-term engagement.

4. Enabling Scalable and Flexible Solutions

AI systems are inherently scalable. Whether you're a startup or an enterprise, AI solutions can grow with your business:

Cloud-based AI platforms offer flexibility and on-demand scaling.

Modular AI systems allow businesses to expand functionalities as needed.

Custom AI applications can be tailored for industry-specific use cases.

This adaptability ensures your business is always equipped to meet changing demands.

5. Strengthening Security and Compliance

Security threats and regulatory pressures continue to rise. AI can help organizations safeguard their data and ensure compliance:

AI-driven security systems detect unusual behavior and potential breaches.

Compliance automation tools help track and report regulatory adherence.

Machine learning models improve fraud detection in real-time.

These proactive security measures protect business integrity and customer trust.

6. Fostering Innovation and Competitive Advantage

AI empowers companies to innovate faster:

AI tools help in product development by analyzing user needs and testing variations.

Businesses can explore new markets with AI-powered market research.

AI accelerates R&D by simulating outcomes and optimizing processes.

Early adopters of AI not only keep up with competitors—they lead the market with smarter, faster innovations.

Conclusion

From operational efficiency and customer satisfaction to data-driven strategies and security, AI software development services offer immense value across every facet of a business. The integration of intelligent technology isn’t just a tech upgrade—it’s a strategic shift toward a more agile, innovative, and future-ready enterprise.

If you’re looking to unlock new growth opportunities, investing in AI software development services is one of the smartest business moves you can make today.

0 notes

Text

Prosthetics and Orthotics Market: Innovations, Accessibility, and Growth Trends Shaping the Future of Mobility

Market Overview

The prosthetics and orthotics market are projected to be valued at USD 7.31 billion in 2025 and is expected to reach USD 9.42 billion by 2030, growing at a compound annual growth rate (CAGR) of 5.2% during the forecast period from 2025 to 2030. Prosthetics are artificial limbs designed to replace missing body parts, while orthotics support and enhance the function of existing limbs or body structures. The market comprises a broad range of products, including lower and upper limb prosthetics, spinal orthoses, and foot and ankle braces. These devices play a critical role in improving patients’ mobility, reducing pain, and enhancing overall quality of life.

Technological innovation, especially in the realm of 3D printing, robotics, and sensor integration, is transforming traditional prosthetic and orthotic solutions into highly sophisticated medical devices tailored to individual needs.

Key Trends Driving the Market

Advances in 3D Printing and Digital Modeling 3D printing has revolutionized the prosthetics and orthotics industry by enabling cost-effective, custom-fit devices. Digital modeling technologies allow for faster production and improved patient comfort.

Integration of Smart Technologies Smart prosthetics equipped with sensors, AI algorithms, and machine learning can mimic natural limb movements more accurately and adapt to the user's behavior, greatly enhancing functional outcomes.

Growing Focus on Pediatric and Geriatric Populations The aging population is more susceptible to conditions requiring orthotic support such as osteoarthritis, diabetes, and post-stroke rehabilitation. Simultaneously, rising attention to pediatric mobility disorders is expanding the need for early-intervention orthotic devices.

Rise in Diabetes and Vascular Diseases With diabetes-related amputations on the rise globally, particularly in low- and middle-income countries, there is a growing demand for both preventive orthotic devices and post-amputation prosthetic care.

Rehabilitation and Post-Surgery Support Increasing use of orthoses in post-operative rehabilitation and injury management is contributing to steady market growth, especially in sports medicine and trauma care.

Improved Access and Reimbursement Policies Expansion of healthcare coverage, especially in North America and Europe, along with supportive reimbursement policies, is helping more patients afford high-quality prosthetic and orthotic devices.

Competitive Landscape

The market includes key players such as Össur, Hanger Inc., Ottobock, Fillauer LLC, and Blatchford Ltd., who continue to invest in R&D to develop lightweight, energy-efficient, and responsive devices. Collaborations with tech companies and research institutions are also driving innovation in bionic limbs and neuroprosthetics.

Additionally, smaller startups are gaining attention by offering modular, affordable solutions through direct-to-consumer channels, particularly in underserved regions.

Regional Insights

North America holds the largest market share due to a strong healthcare infrastructure, high amputation rates, and rapid adoption of new technologies. Europe follows with well-established rehabilitation services and supportive public healthcare systems.

The Asia-Pacific region is witnessing rapid growth, driven by an increasing diabetic population, rising disability awareness, and government investments in public health infrastructure. Countries like India and China are focusing on improving access to mobility aids through public-private partnerships and affordable care models.

Conclusion

The prosthetics and orthotics market is poised for meaningful progress, with a future centered on customization, connectivity, and affordability. Continued innovation in biomaterials, AI, and neurofeedback systems will make next-generation prosthetic and orthotic devices even more life-changing.

As social and economic barriers to access continue to be addressed, the industry is not only expanding but also becoming more inclusive—offering millions of individuals the opportunity to regain independence, functionality, and dignity through modern mobility solutions.

Read More

About Mordor Intelligence:

Mordor Intelligence is a trusted partner for businesses seeking comprehensive and actionable market intelligence. Our global reach, expert team, and tailored solutions empower organizations and individuals to make informed decisions, navigate complex markets, and achieve their strategic goals.

With a team of over 550 domain experts and on-ground specialists spanning 150+ countries, Mordor Intelligence possesses a unique understanding of the global business landscape. This expertise translates into comprehensive syndicated and custom research reports covering a wide spectrum of industries, including aerospace & defense, agriculture, animal nutrition and wellness, automation, automotive, chemicals & materials, consumer goods & services, electronics, energy & power, financial services, food & beverages, healthcare, hospitality & tourism, information & communications technology, investment opportunities, and logistics.

For any inquiries or to access the full report, please contact:

[email protected] https://www.mordorintelligence.com/

0 notes

Text

Programmable Logic Controller Market Set to Hit US$ 17.2 Bn with Strong Demand from Smart Industries

The global programmable logic controller (PLC) market, valued at US$ 11.6 Bn in 2022, is forecast to grow at a CAGR of 4.7% between 2023 and 2031, reaching a market value of US$ 17.2 Bn by the end of 2031, according to the latest industry insights. This growth is propelled by a surge in demand for industrial automation, smart manufacturing, and increased integration of the Industrial Internet of Things (IIoT).

Market Overview: A programmable logic controller (PLC) is a digital computer used to automate electromechanical processes, particularly in manufacturing environments. These devices are integral to the efficient operation of assembly lines, robotic devices, and any activity requiring high-reliability control and ease of programming. With increasing adoption across automotive, food & beverage, chemical, energy & utility, and construction industries, the global PLC market continues to expand in scope and application.

Market Drivers & Trends

The rising trend of smart factories and Industry 4.0 is among the most significant growth drivers. Manufacturers are increasingly adopting automation to reduce operational costs, improve productivity, and enhance precision. PLCs play a critical role in this transformation by allowing control over complex industrial processes with minimal human intervention.

Additionally, the growing need for data-driven decision-making, along with advancements in machine learning and artificial intelligence, is leading to deeper integration of PLCs in industrial settings. As automation becomes central to production and operational strategies, the demand for PLCs is expected to surge further.

Latest Market Trends

One of the most notable trends is the shift toward modular PLCs, which accounted for over 68.2% of the market share in 2022. These PLCs are gaining popularity due to their scalability and suitability for large-scale, complex automation tasks. Modular systems offer higher flexibility, can handle thousands of inputs/outputs, and support multitasking environments—making them ideal for high-volume manufacturing operations.

Another trend is the miniaturization of PLCs, which supports their deployment in compact systems and small machinery, especially in consumer electronics and smaller automated units.

Key Players and Industry Leaders

The competitive landscape is fragmented yet dominated by global industrial automation giants. Leading companies in the PLC market include:

Siemens

Rockwell Automation

Mitsubishi Electric Corporation

Schneider Electric

OMRON Corporation

ABB

Panasonic Corporation

Bosch Rexroth Corporation

Delta Electronics, Inc.

Honeywell International Inc.

These companies continue to drive innovation through strategic partnerships, R&D investments, and product expansions to enhance their market share and global footprint.

Recent Developments

Crouzet, in December 2022, launched Millennium Slim, the slimmest PLC in the world, tailored for compact industrial applications.

In July 2022, OMRON Corporation introduced the CP2E Micro PLC, designed for smaller devices and capable of data collection and machine-to-machine communication. This supports low-cost automation solutions for small- and mid-sized enterprises.

Electronics Corporation of India Limited (ECIL) released its own PLC and SCADA software in May 2022, targeting industrial control applications in Indian manufacturing ecosystems.

These product introductions underline the market’s commitment to technological advancement and responsiveness to evolving industrial demands.

Market Opportunities

The expansion of material handling systems, especially in e-commerce logistics, warehousing, and food processing industries, presents substantial growth potential for PLC integration. In material handling, PLCs streamline storage, movement, and tracking—drastically improving throughput and inventory management.

Additionally, the increasing popularity of energy-efficient manufacturing and sustainability initiatives provides ample opportunity for advanced PLC systems that help monitor and reduce energy consumption across production lines.

Gain a preview of important insights from our Report in this sample - https://www.transparencymarketresearch.com/sample/sample.php?flag=S&rep_id=32672

Future Outlook

The future of the programmable logic controller market lies in enhanced interoperability, cloud integration, and edge computing. With greater reliance on smart infrastructure and connected devices, PLCs are expected to evolve into more intelligent, connected controllers.

The incorporation of AI-powered PLCs is expected to revolutionize industrial automation by enabling predictive maintenance, self-diagnosis, and adaptive process control. As PLCs continue to advance, their use will extend beyond industrial sectors into smart cities, transportation systems, and building automation.

Market Segmentation

By Offering:

Hardware: CPU, I/O Modules, Power Supply, Memory System

Software

Services

By Type:

Compact PLC

Modular PLC

Nano, Micro, Small, Medium, and Large PLCs

By Application:

Material Handling

Packaging & Labeling

Process Control

Safety Monitoring

Energy Management

Home & Building Automation

Industrial Equipment Control

By End-use Industry:

Automotive

Energy & Utilities

Food & Beverage

Pharmaceuticals

Construction

Oil & Gas

Semiconductors & Electronics

Regional Insights

Asia Pacific held the largest market share of 36.3% in 2022, led by strong industrial growth in China, Japan, South Korea, and India. The increasing demand for smart manufacturing systems and compact automation solutions in the region is expected to maintain its dominance through 2031.

North America, with a market share of 26.4% in 2022, continues to grow due to early adoption of factory automation and significant investment in smart infrastructure in the U.S. and Canada.

Europe remains a hub for automation technology innovation, with countries like Germany, the U.K., and France focusing on Industry 4.0 implementation across automotive and manufacturing sectors.

Why Buy This Report?

This comprehensive report offers:

Detailed market size, forecast, and growth rate

In-depth competitive landscape and company profiling

Analysis of key market drivers, trends, and opportunities

Region-wise breakdown for strategic decision-making

Porter’s Five Forces, value chain, and trend analysis

Insights into technological developments and their impact

Market segmentation for customized investment strategies

With expert analysis and forward-looking insights, this report serves as a valuable resource for stakeholders, investors, industrial engineers, and policymakers seeking to navigate and capitalize on the fast-evolving programmable logic controller market.

Explore Latest Research Reports by Transparency Market Research: 5G Smart Antenna Market: https://www.transparencymarketresearch.com/5g-smart-antenna-market.html

Solid State Transformer Market: https://www.transparencymarketresearch.com/solid-State-transformer.html

Interactive Display Market: https://www.transparencymarketresearch.com/interactive-display-market.html

GaN Epitaxial Wafers Market: https://www.transparencymarketresearch.com/gan-epitaxial-wafers-market.html

About Transparency Market Research Transparency Market Research, a global market research company registered at Wilmington, Delaware, United States, provides custom research and consulting services. Our exclusive blend of quantitative forecasting and trends analysis provides forward-looking insights for thousands of decision makers. Our experienced team of Analysts, Researchers, and Consultants use proprietary data sources and various tools & techniques to gather and analyses information. Our data repository is continuously updated and revised by a team of research experts, so that it always reflects the latest trends and information. With a broad research and analysis capability, Transparency Market Research employs rigorous primary and secondary research techniques in developing distinctive data sets and research material for business reports. Contact: Transparency Market Research Inc. CORPORATE HEADQUARTER DOWNTOWN, 1000 N. West Street, Suite 1200, Wilmington, Delaware 19801 USA Tel: +1-518-618-1030 USA - Canada Toll Free: 866-552-3453 Website: https://www.transparencymarketresearch.com Email: [email protected]

0 notes

Text

Top 7 Reasons to Choose KanhaSoft for AI‑Powered CRM & ERP Development in 2025

1. Cutting‑Edge AI Integration: Stay Ahead of CRM & ERP Trends

In 2025, AI integration into CRM and ERP systems has moved from trend to business imperative. From predictive analytics to conversational interfaces, AI-Enabled platforms are now essential.

At KanhaSoft, we embed AI deeply into both CRM and ERP — implementing:

Predictive lead scoring and customer forecasting

AI-driven workflows and task automation

Conversational UIs and chatbots for real-time assistance

Agent‑based autonomous agents handling high-volume tasks

This creates responsive, intelligent systems that act proactively, not just reactively.

2. Tailored, Customizable Solutions That Scale

In emerging markets, one-size-fits-all no longer works. As we’ve highlighted, custom ERP/CRM platforms provide your “secret sauce” — tailoring workflows, data fields, and integrations to your business logic.

KanhaSoft offers:

Low-code/no-code modules supported with AI‑assistance

Rapid customization to match unique industry processes

Scalable architecture that grows with your business

Our approach ensures your system matches your brand, not the other way around.

3. AI-Driven Automation: Efficiency Meets Accuracy

Manual tasks like invoice processing, lead nurturing, and reporting are now AI‑driven. KanhaSoft equips your CRM & ERP with AI

Robotic process automation (RPA) + AI for complex workflows

Automated email/SMS marketing, follow-ups, and segmentation

Enhanced accuracy — AI reduces human error and ensures compliance

This enables your teams to focus on strategic growth rather than repetitive admin tasks.

4. Predictive & Prescriptive Analytics for Informed Decisions

Modern enterprises count on intelligence that goes beyond analytics — to predictions and prescriptions. AI‑powered ERP / AI‑powered CRM provides:

Demand forecasting, inventory optimization, and supply chain

Customer intent prediction, churn prevention, and revenue opportunity insights

Our dashboards offer actionable insights that turn data into growth.

5. Enterprise-Grade Scalability & Integration

Whether you’re operating in a cloud-first or hybrid setup, KanhaSoft delivers:

Cloud or on‑prem deployments, optimized for performance

Open-API & micro-services architecture — easy integration with e-commerce, ERP, BI tools, and more

Modular, microservices-based builds ensuring scalability and adaptability

Your CRM/ERP grows with your business — not constraining it.

6. Robust Security, Compliance & Governance

Security is non-negotiable in 2025. Our systems include:

Encryption, RBAC & MFA for sensitive data

Audit trails and compliance-ready features (GDPR, CCPA, SOC2, etc.)

Governance frameworks for ethical and transparent AI

7. Trusted Partnership & Support Backed by Domain Expertise

KanhaSoft brings over a decade of experience across industries — logistics, real estate, healthcare, manufacturing, and more. Our strengths include:

Domain-specific templates — like Shopify integration, real-estate portals, etc.

Full-cycle services — from architecture and AI training to deployment and support

Transparent SLAs and 24/7 support with dedicated account managers

Conclusion & Call‑to‑Action

In 2025, AI‑powered CRM & ERP systems are no longer optional — they’re essential. By partnering with KanhaSoft, you gain:

AI‑filled intelligence at every level

Scalable, customized platforms tailored to your business

Efficiency through automation

Strategic benefit from analytics

Enterprise-grade integration

Security-first practices

Ongoing support from domain experts

If your business aims to future-proof operations with intelligent, scalable, and secure software, let’s connect. Discover how KanhaSoft can build the next-gen AI‑CRM & ERP solution built for your success.

0 notes

Text

What’s Next in ERP & CRM? Trends to Watch in 2025 and Beyond

As businesses continue to accelerate digital transformation in the post-pandemic world, Enterprise Resource Planning (ERP) and Customer Relationship Management (CRM) systems are evolving faster than ever. What used to be back-end support systems have now become the core engines driving operational efficiency, customer experience, and innovation.

In 2025 and beyond, ERP and CRM platforms are expected to move beyond traditional functionality into smarter, more integrated ecosystems that empower data-driven decisions, automation, and predictive performance. Whether you’re a CIO looking to modernize legacy systems or a business leader exploring tech-driven growth, understanding the upcoming trends is crucial to staying competitive.

So, what’s next in ERP and CRM? Let’s dive into the future.

The New Era of ERP & CRM

Legacy, siloed software is on its way out. Today’s ERP and CRM systems are cloud-native, mobile-first, and AI-powered. They’re no longer just tools — they’re strategic assets. Organizations are looking for smarter ways to manage their operations and customer relationships in a unified, real-time environment.

Key shifts driving this transformation include:

The rise of cloud-based ERP and CRM platforms

AI and machine learning integration for real-time intelligence

Emphasis on modularity, flexibility, and scalability

The convergence of ERP and CRM for a 360-degree business view

Top ERP Trends to Watch in 2025

1.AI-Powered ERP Becomes the Norm

Artificial intelligence is transforming ERP systems from reactive databases into predictive, self-learning platforms. Expect AI to optimize supply chain management, automate financial forecasting, and predict equipment maintenance.

Key Benefits:

Enhanced decision-making with predictive analytics

Reduced human error through intelligent automation

Smarter resource planning and budgeting

2.Composable and Modular ERP Architecture

Gone are the days of one-size-fits-all ERP suites. Businesses in 2025 will adopt composable ERP systems that allow modules to be added or removed based on specific needs.

Why It Matters:

Faster implementation

Lower total cost of ownership (TCO)

Flexibility across departments and geographies

3.Cloud-First ERP Deployment

Cloud ERP systems like SAP S/4HANA, Oracle Cloud ERP, and NetSuite continue to dominate due to their agility, scalability, and cost-efficiency.

Trends to Watch:

Hybrid-cloud and multi-cloud ERP environments

Improved uptime and data security

Remote accessibility for global teams

4.ERP for SMEs: Simpler, Smarter, Faster

Small and medium businesses are embracing affordable cloud ERP solutions with built-in automation, intuitive dashboards, and minimal setup time.

What’s Changing:

Low-code customization

Industry-specific templates

Shorter deployment cycles

5.Hyperautomation Through RPA

Robotic Process Automation (RPA) will continue to integrate with ERP platforms to handle repetitive tasks, freeing up human resources for strategic work.

Top CRM Trends to Watch in 2025

1.AI-Driven Personalization at Scale

AI in CRM is moving beyond basic lead scoring. Expect hyper-personalization with real-time behavioral tracking, sentiment analysis, and dynamic content delivery.

Examples:

Personalized email journeys

AI-recommended products and services

Real-time chatbot support

2.Voice-Enabled and Conversational CRM

With natural language processing (NLP) advancements, CRM systems are becoming conversational. Sales reps can update records, schedule meetings, and get reports via voice.

Voice Integration Channels:

Alexa for Business

Google Assistant for CRM updates

Smart voice dashboards

3.Omnichannel Customer Engagement

In 2025, customers expect seamless interactions across channels — web, mobile, social, email, and even offline. CRMs must offer real-time synchronization and unified data tracking.

Key Features to Expect:

Unified inbox for all communication

Real-time notifications for lead interactions

Journey-based automation workflows

4.CRM + Data Analytics = Revenue Growth

Modern CRMs aren’t just for managing contacts — they’re growth engines. Integrated BI dashboards help sales and marketing teams align, prioritize leads, and track performance.

Impactful Insights:

Conversion funnel analysis

Attribution modeling

Churn prediction

5.CRM Meets IoT, AR & Metaverse

Advanced CRM systems are beginning to integrate with IoT devices and AR/VR platforms to create immersive customer experiences.

Emerging Use Cases:

IoT data integration for personalized service

AR-powered product demos

Virtual storefronts in the metaverse

ERP + CRM: The Power of Integration

The future of enterprise software lies in seamless integration. Forward-thinking companies are combining ERP and CRM systems into a unified tech stack for holistic business management.

Benefits of ERP-CRM Integration:

One source of truth for customer and financial data

Better collaboration across departments

End-to-end automation of workflows (quote to cash, lead to revenue)

Industry-Specific Innovations

Healthcare:

Patient relationship management + resource scheduling

Integration with EHR systems and telehealth platforms

Manufacturing:

Real-time production tracking

Integrated quality control and supplier management

Retail & eCommerce:

Inventory and order sync with CRM marketing campaigns

Customer loyalty programs based on real-time data

Finance:

Automated compliance and reporting

Unified customer and transaction insights

Security, Privacy & Compliance

As digital ecosystems grow, so do risks. In 2025, ERP and CRM systems will be embedded with zero-trust security models, data encryption, and compliance modules for GDPR, HIPAA, and other regional laws.

Trends:

Role-based access control (RBAC)

AI-powered fraud detection

Secure APIs and integration layers

Challenges Businesses Must Prepare For

Change Management: Ensuring user adoption and minimizing resistance

Data Migration: Migrating legacy data securely and accurately

Cost vs ROI: Balancing budget with long-term value

Vendor Lock-in: Choosing platforms with open standards and APIs

What Businesses Should Do Now

To stay ahead of the curve, businesses should:

Audit existing ERP and CRM systems for gaps and opportunities

Invest in AI-ready, cloud-native platforms with strong vendor support

Emphasize integration and interoperability

Prioritize user experience and mobile accessibility

Train staff continuously to adapt to evolving tools

Conclusion

ERP and CRM platforms are no longer just enterprise software — they are the digital backbone of modern business. As we step into 2025 and beyond, companies that embrace intelligent, cloud-powered, and integrated systems will be the ones that lead.

Whether you’re planning a full transformation or small-scale modernization, now is the time to act.

0 notes

Text

Zero-Waste Strategies in Construction for Green Building Goals

The construction industry has long grappled with the challenge of waste generation. From unused materials to packaging and demolition debris, the environmental footprint of construction sites continues to grow. However, zero-waste strategies in construction are reshaping the future of building by focusing on sustainable methods, efficient resource use, and waste elimination. These strategies not only reduce landfill loads but also enhance project cost-effectiveness, site cleanliness, and overall industry accountability.

Understanding Zero-Waste in Construction Zero-waste in construction refers to the systematic effort to prevent and eliminate waste through smarter design, efficient material usage, and responsible disposal. It emphasizes a circular economy approach where resources are continually reused and repurposed, and nothing is sent to landfill unnecessarily. Rather than viewing leftover materials as inevitable, zero-waste thinking encourages planning and design strategies that prevent waste from the beginning.

Designing for Material Efficiency One of the foundational steps in minimizing construction waste is intelligent design. By adopting modular construction, prefabricated components, and precise measurement planning, builders can significantly cut down on excess materials. Advanced software tools assist architects and engineers in optimizing material layouts and reducing off-cuts and errors. The use of Building Information Modeling (BIM) also allows teams to identify potential waste sources during the design phase and adjust before construction begins.

On-Site Waste Reduction Techniques Efficient inventory management is essential to avoid over-ordering materials. Labeling, storing, and protecting materials properly ensures that fewer resources go to waste due to weather exposure or mishandling. Just-in-time delivery practices limit the volume of materials stored on-site, further preventing damage or theft. Workers should be trained to segregate waste immediately into designated streams like wood, metal, concrete, and packaging, which enables better recycling and reuse.

Recycling and Reuse in Real-Time Reusing and recycling materials as they are removed from the site helps lower waste volume significantly. Demolition waste such as concrete, bricks, and metals can often be crushed or melted down and reused. Donating unused or lightly used materials to community projects or salvage companies also contributes to the zero-waste cycle. Establishing partnerships with local recycling facilities or waste processors ensures consistent material recovery.

Training and Stakeholder Engagement Achieving zero-waste outcomes requires collaboration from all parties involved in a construction project. Contractors, site managers, suppliers, and laborers must be trained on sustainable practices and the importance of waste reduction. Regular team meetings, performance tracking, and incentive programs can motivate everyone to stay aligned with zero-waste goals. Clear communication and accountability make these practices part of the construction site culture.

Technology’s Role in Minimizing Waste Emerging technologies are enabling smarter waste tracking and reduction strategies. Mobile apps can log material usage and waste output in real time, offering instant feedback to teams. AI-powered systems help forecast material demand and usage rates, helping avoid over-ordering. Robotics and 3D printing allow for precision manufacturing, cutting down significantly on material waste and enhancing sustainability.

Monitoring, Reporting, and Continuous Improvement Monitoring waste reduction metrics is essential to track progress. Reporting platforms allow construction teams to assess performance, identify areas of inefficiency, and adapt accordingly. Periodic waste audits, feedback sessions, and sustainability reports help refine strategies and achieve continuous improvement. These data-driven insights are key to evolving a zero-waste strategy into standard practice.

For more info https://bi-journal.com/zero-waste-strategies-to-cut-construction-site/

Conclusion Zero-waste strategies in construction are no longer optional but essential in creating environmentally responsible and economically efficient projects. From design through delivery, each step in the building process presents opportunities to cut waste and enhance sustainability. By adopting smart technologies, training teams, and maintaining clear goals, construction sites can transition from waste-heavy operations to zero-waste leaders. The path forward is built on innovation, commitment, and a collective drive to protect resources and the planet.

#zero-waste#sustainable construction#green construction#bi-journal news#bi-journal services#business insight journal

0 notes

Text

Medical Exoskeletons Surge to $5.8B by 2034 🤖💪 | CAGR: 17.1%

Medical Exoskeleton Market is poised for exponential growth, expected to surge from $1.2 billion in 2024 to $5.8 billion by 2034, at an impressive CAGR of 17.1%. These wearable robotic systems are transforming patient rehabilitation and mobility support, offering new hope for individuals with spinal cord injuries, stroke complications, and age-related impairments. By enhancing muscle strength and limb movement, medical exoskeletons are revolutionizing how care is delivered in clinical and home settings.

Market Dynamics

Driving this dynamic market are technological advancements in robotics, AI integration, and lightweight materials. The increasing prevalence of mobility disorders, a rapidly aging population, and the growing demand for non-invasive assistive solutions have significantly amplified the adoption of medical exoskeletons.

Click to Request a Sample of this Report for Additional Market Insights: https://www.globalinsightservices.com/request-sample/?id=GIS24850

While the lower body exoskeleton segment dominates with over 55% of the market share, upper body and full body models are gaining momentum. Innovations like intuitive control systems, battery efficiency, and reduced device weight are pushing boundaries in comfort and performance. However, high production costs and stringent regulatory frameworks remain hurdles, necessitating a balance between affordability and technological sophistication.

Key Players Analysis

Key industry players are leading innovation and shaping competitive dynamics.��Ekso Bionics and ReWalk Robotics stand out for their clinically adaptive devices, while Cyberdyne Inc. continues to push forward with its cutting-edge HAL systems. Other notable companies include Bionik Laboratories, Hocoma, and Ottobock, each contributing to an expanding ecosystem of therapeutic and assistive technologies.

Emerging players such as Neuro Stride, Rehab Tech Innovations, and Stride Forward are also making their mark by focusing on niche clinical needs and cost-effective solutions. These companies are leveraging R&D partnerships and digital health integrations to tap into underserved segments.

Regional Analysis

North America leads the global market, fueled by robust R&D investments, advanced healthcare infrastructure, and early technology adoption, with the U.S. being a critical growth engine. Europe follows closely, particularly in Germany and the UK, where government-backed initiatives support rehabilitation-focused innovations.

In Asia-Pacific, countries like Japan and China are witnessing increased uptake due to rising healthcare investments and demographic shifts. The region’s fast-growing elderly population is creating fertile ground for expansion.

Meanwhile, Latin America and the Middle East & Africa represent emerging frontiers. Though adoption is currently slower, increasing awareness and policy support are paving the way for accelerated growth.

Recent News & Developments

Recent developments have seen the integration of AI and machine learning into exoskeletons, enhancing real-time motion adjustments and user feedback. Companies are also adopting modular designs and IoT connectivity to broaden usability. Notably, military and industrial applications are gaining traction, diversifying the market’s reach beyond traditional healthcare settings.

Pricing remains a complex issue, with premium models offering advanced functionalities and AI-driven analytics, while budget models aim to expand accessibility. Regulatory shifts in the U.S. and EU are shaping how companies innovate and bring products to market, emphasizing safety, efficacy, and cost-effectiveness.

Browse Full Report : https://www.globalinsightservices.com/reports/medical-exoskeleton-market/

Scope of the Report

This comprehensive report offers an in-depth view of the medical exoskeleton market, covering historical trends (2018–2023), the base year (2024), and a detailed forecast (2025–2034). It provides a segmented analysis across product types, components, end-users, technologies, and regions. The report evaluates market drivers, restraints, opportunities, and threats, while offering a competitive landscape overview, strategic profiling of major players, and SWOT and PESTLE analyses.

With thorough data from organizations such as WHO, FDA, EMA, and global tech conferences, this research empowers stakeholders with the insights needed to make informed decisions, mitigate risks, and seize growth opportunities in a rapidly evolving landscape.

Discover Additional Market Insights from Global Insight Services:

Ophthalmology Contract Research Organization (CRO) Market is anticipated to expand from $4.2 billion in 2024 to $8.9 billion by 2034, growing at a CAGR of approximately 7.8%.

Infectious Disease Diagnostics Market is anticipated to expand from $38.5 billion in 2024 to $72.3 billion by 2034, growing at a CAGR of approximately 6.5%.

Laboratory Information Management System (LIMS) Market is anticipated to expand from $2.1 billion in 2024 to $4.5 billion by 2034, growing at a CAGR of approximately 7.9%.

Orthopedic Braces & Supports Market is anticipated to expand from $4.2 billion in 2024 to $7.9 billion by 2034, growing at a CAGR of approximately 6.5%.

Breast Reconstruction Market is anticipated to expand from $3.2 billion in 2024 to $5.8 billion by 2034, growing at a CAGR of approximately 6.1%.

About Us:

Global Insight Services (GIS) is a leading multi-industry market research firm headquartered in Delaware, US. We are committed to providing our clients with highest quality data, analysis, and tools to meet all their market research needs. With GIS, you can be assured of the quality of the deliverables, robust & transparent research methodology, and superior service.

Contact Us:

Global Insight Services LLC 16192, Coastal Highway, Lewes DE 19958 E-mail: [email protected] Phone: +1–833–761–1700 Website: https://www.globalinsightservices.com/

0 notes

Text

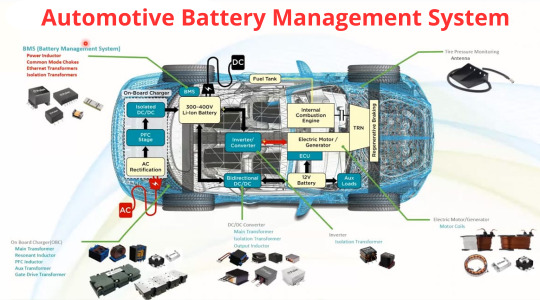

Automotive Battery Management System Market Size, Analyzing Trends and Projected Outlook for 2025-2032

Fortune Business Insights released the Global Automotive Battery Management System Market Trends Study, a comprehensive analysis of the market that spans more than 150+ pages and describes the product and industry scope as well as the market prognosis and status for 2025-2032. The marketization process is being accelerated by the market study's segmentation by important regions. The market is currently expanding its reach.

The Automotive Battery Management System Market is experiencing robust growth driven by the expanding globally. The Automotive Battery Management System Market is poised for substantial growth as manufacturers across various industries embrace automation to enhance productivity, quality, and agility in their production processes. Automotive Battery Management System Market leverage robotics, machine vision, and advanced control technologies to streamline assembly tasks, reduce labor costs, and minimize errors. With increasing demand for customized products, shorter product lifecycles, and labor shortages, there is a growing need for flexible and scalable automation solutions. As technology advances and automation becomes more accessible, the adoption of automated assembly systems is expected to accelerate, driving market growth and innovation in manufacturing. Automotive Battery Management System Market Size, Share & Industry Analysis, By Type (Lithium-ion, Lead Acid, Nickel-based), By Connection Topology (Centralized , Distributed , Modular), By Vehicle type (Electric Vehicles, E-bikes) And Regional Forecast 2021-2028

Get Sample PDF Report: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/105479

Major Automotive Battery Management System Market Manufacturers covered in the market report include:

Some of the major companies that are present in the automotive battery management system market include Thyssenkrupp AG, Nippon Steel Integrated Battery Management LLC, Braynt Racing Inc., Arrow Precision Ltd., Maschinenfabrik Alfing Kessler GmbH, Mahindra CIE, Tianrun Battery Management Co., Ltd., among others.

Owing to this, many Battery Management manufacturers are developing advanced Battery Management with improved fatigue strength, reliability, and quality. Also, the crankshafts are manufactured with the latest trend of steelmaking processes by materials with high strength, and this factor is also expected to drive the automotive Battery Management market.

Geographically, the detailed analysis of consumption, revenue, market share, and growth rate of the following regions:

The Middle East and Africa (South Africa, Saudi Arabia, UAE, Israel, Egypt, etc.)

North America (United States, Mexico & Canada)

South America (Brazil, Venezuela, Argentina, Ecuador, Peru, Colombia, etc.)

Europe (Turkey, Spain, Turkey, Netherlands Denmark, Belgium, Switzerland, Germany, Russia UK, Italy, France, etc.)

Asia-Pacific (Taiwan, Hong Kong, Singapore, Vietnam, China, Malaysia, Japan, Philippines, Korea, Thailand, India, Indonesia, and Australia).

Automotive Battery Management System Market Research Objectives:

- Focuses on the key manufacturers, to define, pronounce and examine the value, sales volume, market share, market competition landscape, SWOT analysis, and development plans in the next few years.

- To share comprehensive information about the key factors influencing the growth of the market (opportunities, drivers, growth potential, industry-specific challenges and risks).

- To analyze the with respect to individual future prospects, growth trends and their involvement to the total market.

- To analyze reasonable developments such as agreements, expansions new product launches, and acquisitions in the market.

- To deliberately profile the key players and systematically examine their growth strategies.

Frequently Asked Questions (FAQs):

► What is the current market scenario?

► What was the historical demand scenario, and forecast outlook from 2025 to 2032?

► What are the key market dynamics influencing growth in the Global Automotive Battery Management System Market ?

► Who are the prominent players in the Global Automotive Battery Management System Market ?

► What is the consumer perspective in the Global Automotive Battery Management System Market ?

► What are the key demand-side and supply-side trends in the Global Automotive Battery Management System Market ?

► What are the largest and the fastest-growing geographies?

► Which segment dominated and which segment is expected to grow fastest?

► What was the COVID-19 impact on the Global Automotive Battery Management System Market ?

FIVE FORCES & PESTLE ANALYSIS:

In order to better understand market conditions five forces analysis is conducted that includes the Bargaining power of buyers, Bargaining power of suppliers, Threat of new entrants, Threat of substitutes, and Threat of rivalry.

Political (Political policy and stability as well as trade, fiscal, and taxation policies)

Economical (Interest rates, employment or unemployment rates, raw material costs, and foreign exchange rates)

Social (Changing family demographics, education levels, cultural trends, attitude changes, and changes in lifestyles)

Technological (Changes in digital or mobile technology, automation, research, and development)

Legal (Employment legislation, consumer law, health, and safety, international as well as trade regulation and restrictions)

Environmental (Climate, recycling procedures, carbon footprint, waste disposal, and sustainability)

Points Covered in Table of Content of Global Automotive Battery Management System Market :

Chapter 01 - Automotive Battery Management System Market for Automotive Executive Summary

Chapter 02 - Market Overview

Chapter 03 - Key Success Factors

Chapter 04 - Global Automotive Battery Management System Market - Pricing Analysis

Chapter 05 - Global Automotive Battery Management System Market Background or History

Chapter 06 - Global Automotive Battery Management System Market Segmentation (e.g. Type, Application)

Chapter 07 - Key and Emerging Countries Analysis Worldwide Automotive Battery Management System Market .

Chapter 08 - Global Automotive Battery Management System Market Structure & worth Analysis

Chapter 09 - Global Automotive Battery Management System Market Competitive Analysis & Challenges

Chapter 10 - Assumptions and Acronyms